Markets are opening Friday with one big question: does the labor market still look too strong for a quick easing cycle, especially while global energy risk stays elevated?

What happened

The U.S. Bureau of Labor Statistics’ latest Employment Situation release showed payroll growth of 130,000 in January and an unemployment rate of 4.3%. Wage and labor details remain central because they influence how quickly inflation can cool. In other words, investors are not looking at one headline number; they are looking at whether labor demand is easing enough to reduce price pressure over time.

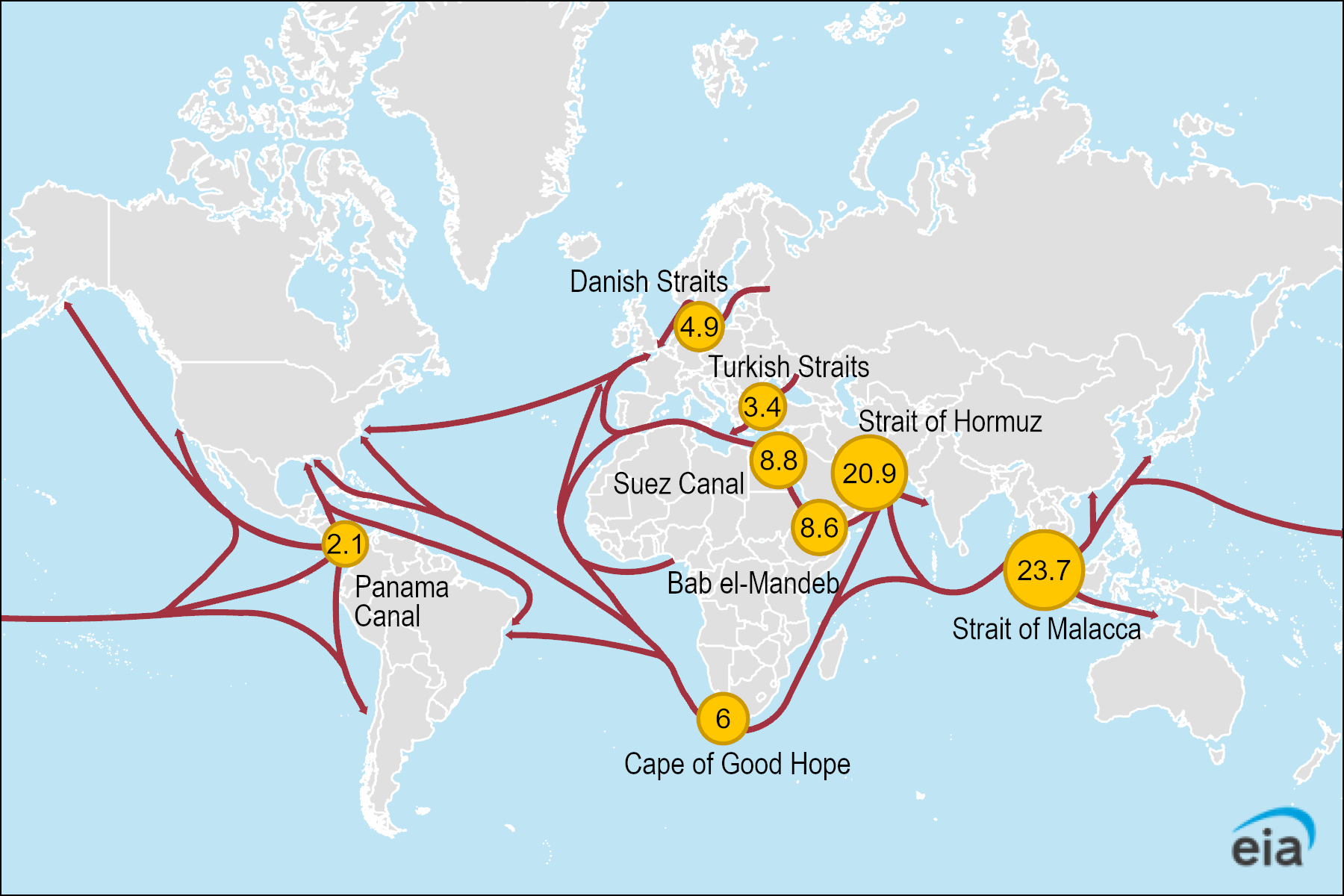

At the same time, global energy remains part of the macro story. Recent U.S. EIA updates highlight shifting global supply dynamics, including LNG contract activity and changes in power generation trends across countries. Even when there is no immediate supply disruption, markets price the risk that geopolitical tension or shipping bottlenecks could keep oil and energy costs volatile.

That creates a two-layer setup: domestic labor data on one side, global energy uncertainty on the other.

Why it matters

For everyday market followers, this matters because interest-rate expectations are the bridge between macro data and asset prices.

- If jobs and wage momentum stay firm, investors may expect central banks to keep policy tighter for longer.

- If energy costs remain jumpy, inflation expectations can stay sticky even if some domestic indicators soften.

- When both forces happen together, markets can reprice quickly across stocks, bonds, and currencies.

Put simply: this is less about drama and more about probability. Markets are constantly updating odds for future rate cuts, and those odds are highly sensitive to labor and energy signals right now.

There is also a world-agenda angle that matters beyond one country. Energy routes, sanctions risk, and geopolitical flashpoints can spill into global inflation through transport and input costs. That means a U.S. jobs day can still be influenced by events far outside U.S. borders.

What to watch next

Over the next week, focus on a short checklist instead of chasing every headline:

- Jobs internals: payrolls, unemployment, and wage growth together.

- Energy trend: whether oil and gas volatility cools or re-accelerates.

- Central-bank tone: whether officials emphasize patience or signal confidence on disinflation.

If you want to follow this without noise, keep a calendar view of key releases and decisions: Track upcoming events in Finovu Calendar.

Bottom line

Friday’s market tone is being set by a simple but powerful combination: labor-market resilience plus global energy risk. As long as both stay active, rate expectations may keep shifting quickly, and market moves can remain choppy even without a single “shock” headline.

Sources